The United States market has seen a positive trajectory, climbing 2.3% over the past week and 5.9% in the last year, with earnings forecasted to grow by 14% annually. In this environment, identifying stocks that may be undervalued can offer potential opportunities for investors seeking to capitalize on growth prospects within smaller companies.

Top 10 Undervalued Small Caps With Insider Buying In The United States

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Shore Bancshares | 9.9x | 2.2x | 12.32% | ★★★★★☆ |

| MVB Financial | 10.8x | 1.5x | 36.61% | ★★★★★☆ |

| Flowco Holdings | 6.1x | 0.9x | 40.71% | ★★★★★☆ |

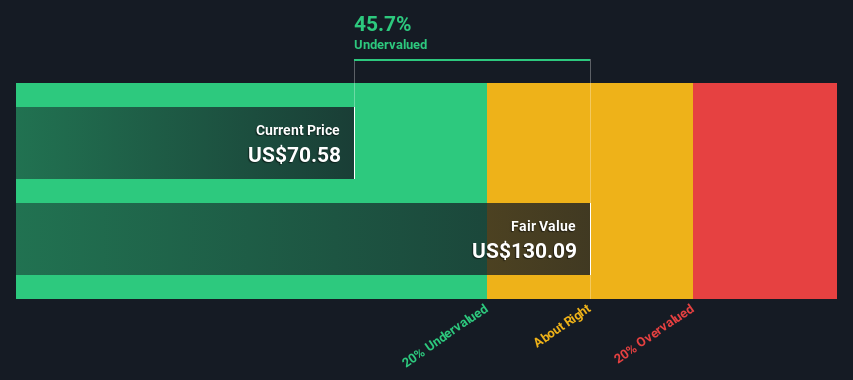

| S&T Bancorp | 10.6x | 3.6x | 44.01% | ★★★★☆☆ |

| Forestar Group | 5.8x | 0.7x | -401.96% | ★★★★☆☆ |

| Columbus McKinnon | 42.1x | 0.4x | 44.29% | ★★★☆☆☆ |

| Franklin Financial Services | 15.9x | 2.6x | 34.96% | ★★★☆☆☆ |

| PDF Solutions | 170.7x | 3.9x | 24.03% | ★★★☆☆☆ |

| Delek US Holdings | NA | 0.1x | -13.95% | ★★★☆☆☆ |

| Titan Machinery | NA | 0.1x | -325.34% | ★★★☆☆☆ |

Let's uncover some gems from our specialized screener.

ArcBest (NasdaqGS:ARCB)

Simply Wall St Value Rating: ★★★★★☆

Overview: ArcBest is a logistics company specializing in providing comprehensive freight transportation services, with operations divided into asset-based and asset-light segments, and has a market capitalization of approximately $2.36 billion.

Operations: The company's revenue primarily comes from its Asset-Based and Asset-Light segments, generating $2.75 billion and $1.55 billion respectively. Over recent periods, the gross profit margin has fluctuated, reaching a high of 14.95% in early 2020 before settling at around 9% by late 2024.

PE: 8.3x

ArcBest, a company navigating the competitive logistics landscape, has recently faced challenges with Nasdaq compliance due to audit committee issues but swiftly regained compliance by adjusting their board composition. Their innovative Vaux Vision technology enhances operational efficiency in material handling, reflecting a commitment to technological advancement. Despite a dip in earnings for 2024, ArcBest's forecasted growth of 3.38% annually suggests potential for future expansion. Insider confidence is bolstered by share repurchases totaling $15.17 million from October 2024 to January 2025, indicating management's belief in the company's value proposition amidst its small-cap characteristics and evolving market strategies.

Bloomin' Brands (NasdaqGS:BLMN)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Bloomin' Brands is a restaurant company that operates several casual dining chains, with a market capitalization of approximately $2.30 billion.

Operations: Bloomin' Brands generates revenue primarily from its operations in the United States, with significant contributions from international franchises. The company's cost of goods sold (COGS) consistently represents a substantial portion of its expenses. Notably, the net income margin has shown variability over time, reflecting fluctuations in profitability.

PE: -13.7x

Bloomin' Brands, known for its restaurant chains, exhibits potential as an undervalued stock despite recent financial challenges. Insider confidence is evident with Michael Spanos purchasing 118,000 shares for US$1.02 million in April 2025. The company reported a net loss of US$128 million for 2024 but expects earnings per share to range from $1.08 to $1.28 in 2025. Despite volatile share prices and high debt levels, strategic leadership changes and insider activity suggest optimism about future performance amidst industry headwinds.

- Unlock comprehensive insights into our analysis of Bloomin' Brands stock in this valuation report.

Gain insights into Bloomin' Brands' past trends and performance with our Past report.

Camping World Holdings (NYSE:CWH)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Camping World Holdings operates as a retailer specializing in recreational vehicles (RVs) and outdoor products, with additional services offered through its Good Sam brand, and has a market capitalization of approximately $1.66 billion.

Operations: The company's revenue is primarily derived from RV and Outdoor Retail, contributing $5.92 billion, with Good Sam Services and Plans adding $195.63 million. Over recent periods, the gross profit margin has shown a declining trend from 35.78% in March 2022 to 29.93% by December 2024. Operating expenses are significant, with General & Administrative Expenses consistently forming a substantial portion of these costs.

PE: -21.0x

Camping World Holdings, a smaller player in the market, has caught attention due to insider confidence with notable share purchases over recent months. Despite facing challenges like a net loss of US$38.64 million for 2024 and reliance on external borrowing, they maintain regular dividends at US$0.125 per share. Revenue hit US$6.1 billion last year, showing resilience amid financial hurdles. Earnings are forecasted to grow annually by 108%, hinting at potential future growth despite current setbacks.

Summing It All Up

- Embark on your investment journey to our 86 Undervalued US Small Caps With Insider Buying selection here.

- Invested in any of these stocks? Simplify your portfolio management with Simply Wall St and stay ahead with our alerts for any critical updates on your stocks.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com