Saia (NASDAQ:SAIA) is set to give its latest quarterly earnings report on Friday, 2025-04-25. Here's what investors need to know before the announcement.

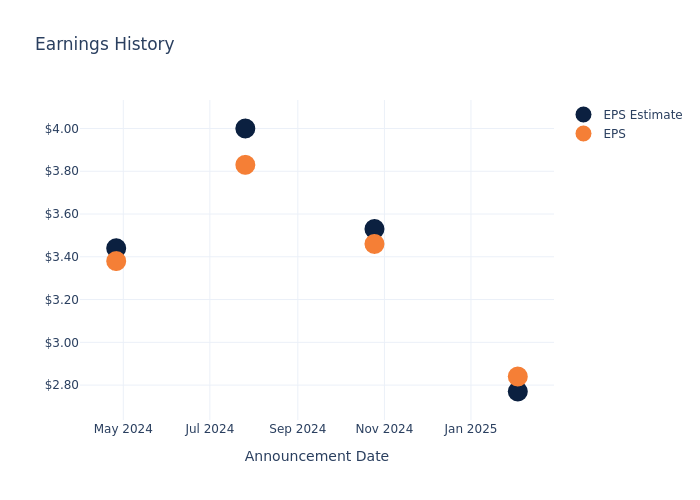

Analysts estimate that Saia will report an earnings per share (EPS) of $2.77.

Saia bulls will hope to hear the company announce they've not only beaten that estimate, but also to provide positive guidance, or forecasted growth, for the next quarter.

New investors should note that it is sometimes not an earnings beat or miss that most affects the price of a stock, but the guidance (or forecast).

Performance in Previous Earnings

In the previous earnings release, the company beat EPS by $0.07, leading to a 1.88% increase in the share price the following trading session.

Here's a look at Saia's past performance and the resulting price change:

| Quarter | Q4 2024 | Q3 2024 | Q2 2024 | Q1 2024 |

|---|---|---|---|---|

| EPS Estimate | 2.77 | 3.53 | 4 | 3.44 |

| EPS Actual | 2.84 | 3.46 | 3.83 | 3.38 |

| Price Change % | 2.0% | 11.0% | -19.0% | -21.0% |

Market Performance of Saia's Stock

Shares of Saia were trading at $341.48 as of April 23. Over the last 52-week period, shares are down 19.49%. Given that these returns are generally negative, long-term shareholders are likely a little upset going into this earnings release.

Analysts' Take on Saia

Understanding market sentiments and expectations within the industry is crucial for investors. This analysis delves into the latest insights on Saia.

The consensus rating for Saia is Buy, based on 21 analyst ratings. With an average one-year price target of $493.48, there's a potential 44.51% upside.

Comparing Ratings with Peers

This comparison focuses on the analyst ratings and average 1-year price targets of and Saia, three major players in the industry, shedding light on their relative performance expectations and market positioning.

Summary of Peers Analysis

Within the peer analysis summary, vital metrics for and Saia are presented, shedding light on their respective standings within the industry and offering valuable insights into their market positions and comparative performance.

| Company | Consensus | Revenue Growth | Gross Profit | Return on Equity |

|---|---|---|---|---|

| Saia | Buy | 5.04% | $147.49M | 3.35% |

Key Takeaway:

Saia is positioned in the middle among its peers based on the consensus rating. It ranks at the bottom for revenue growth, with a growth rate of 5.04%. In terms of gross profit, Saia is at the top with $147.49M. However, its return on equity is at the bottom with 3.35%.

Delving into Saia's Background

Saia ranks among the 10 largest less-than-truckload carriers in the United States, with more than 200 facilities and a fleet of more than 6,500 tractors and 26,000 trailers. As a national LTL carrier, the firm offers time-definite and expedited options for shipments ranging between 100 and 10,000 pounds. Saia ranks among the top-tier providers in terms of profitability.

A Deep Dive into Saia's Financials

Market Capitalization Analysis: The company's market capitalization is above the industry average, indicating that it is relatively larger in size compared to peers. This may suggest a higher level of investor confidence and market recognition.

Revenue Growth: Over the 3 months period, Saia showcased positive performance, achieving a revenue growth rate of 5.04% as of 31 December, 2024. This reflects a substantial increase in the company's top-line earnings. When compared to others in the Industrials sector, the company excelled with a growth rate higher than the average among peers.

Net Margin: Saia's net margin excels beyond industry benchmarks, reaching 9.65%. This signifies efficient cost management and strong financial health.

Return on Equity (ROE): The company's ROE is a standout performer, exceeding industry averages. With an impressive ROE of 3.35%, the company showcases effective utilization of equity capital.

Return on Assets (ROA): Saia's ROA stands out, surpassing industry averages. With an impressive ROA of 2.44%, the company demonstrates effective utilization of assets and strong financial performance.

Debt Management: Saia's debt-to-equity ratio is below industry norms, indicating a sound financial structure with a ratio of 0.14.

To track all earnings releases for Saia visit their earnings calendar on our site.

This article was generated by Benzinga's automated content engine and reviewed by an editor.